When you have terrible credit, you may believe that buying a property is impossible. However, just because you have credit issues does not inevitably imply you will be denied a mortgage.

Despite your low credit, some mortgage lenders may be ready to work with you. The same is true if you’re seeking to purchase a property with no credit. However, your challenges may vary from those faced by those with poor credit ratings.

In this article, we’ll look at what it’s like to purchase a property with bad credit and how much it can cost you.

What Constitutes Poor Credit?

When your credit score or payment history falls short of your lender’s minimal guidelines, you have bad credit.

Some mortgage lenders want a minimum credit score of 500 on a range of 300-850, while others require 580, 620, or higher.

Minimum credit scores vary per lender since lenders aren’t always concerned about your credit score. What they truly worry about is whether or not you will repay them each month.

A mortgage lender uses credit scores as one of several factors. Lenders are also concerned with your work stability, yearly income, the property you’re purchasing, and other factors.

In other words, there is no such thing as negative credit in the eyes of a mortgage lender, but a mortgage is not guaranteed approval loans because to get this type of loan, you need to seriously prepare. There is just qualifying credit, which is the minimum credit score necessary for a mortgage application to be approved.

What is the minimum credit score for purchasing a home?

Credit Ratings Ranging From 500 to 579

In theory, you may get a mortgage with a credit score as low as 500, but you’ll be restricted to loans guaranteed by the Federal Housing Administration. A down payment of at least 10% is required for an FHA loan with a credit score of 500 to 579. Any outstanding collections and judgments will be demanded by the lender.

Credit Ratings Ranging From 580 to 619

You might qualify for an FHA loan with as little as 3.5% down.

Credit Ratings Ranging From 620 to 699

Your mortgage options are expanding. With a credit score of 620, you may be able to qualify for a conventional loan, which is not guaranteed by a government agency like the FHA or VA.

Credit Scores of 700 or Higher

Lenders are more ready to issue credit if your credit score is between 700 and 739, and a score of 740 or above will result in the lowest interest rates.

How to Raise Your Credit Rating

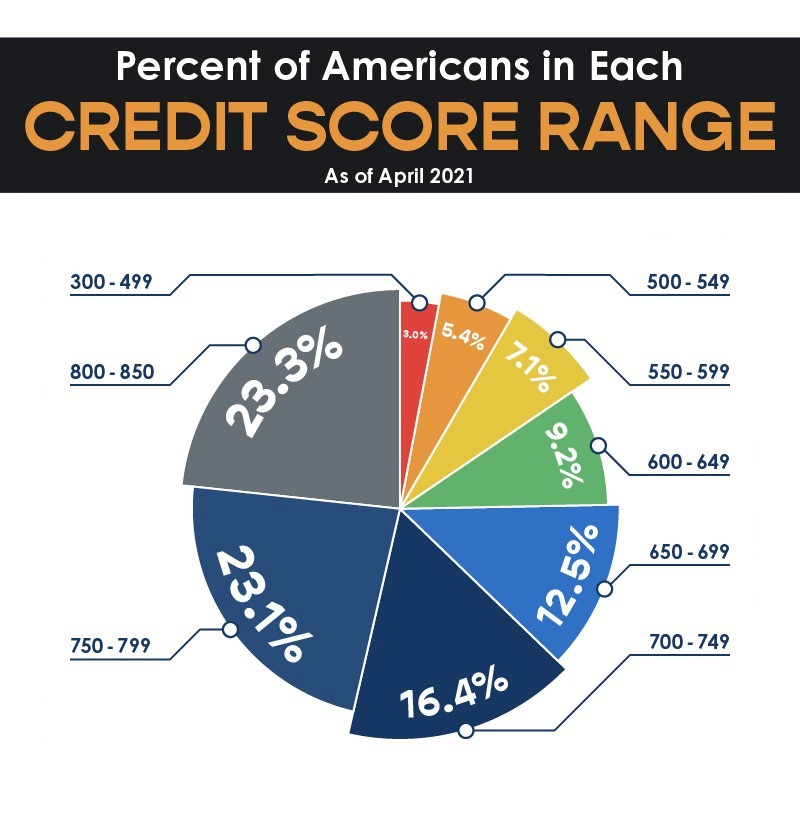

As you can see in the picture, there are fewer people with very bad credit, only 3 percent. But if you are there, then you still have a chance to buy a house.

But if your credit score is less than 580, focus on these financial practices to help raise it.

Enhance Your Payment History

Payment consistency is an important aspect of determining your credit score. With each payment, you will increase your credit history and score if you make frequent on-time payments on your bills.

Reduce Your Entire Debt to Improve Your Debt-to-income Ratio

Your accessible credit also has an impact on your credit score. Improving your credit score will be difficult if you are maxed out and have no credit. Pay off debt to build a credit cushion, and your credit score will climb.

Examine Your Credit Report For Mistakes and File a Dispute

Consider using a credit restoration firm to help you get on track to purchasing a property. When you get your free credit report, you may discover certain inaccuracies that lower your credit score. Significant blemishes on your credit record, such as foreclosures, repossessions, or collections accounts, may have a considerable impact.

Reduce Your Credit Use

Paying off credit cards and other personal loans reduces your credit utilization ratio, which is the total of all your liabilities divided by the limitations on your credit cards. This has a beneficial effect on your debt-to-income ratio (DTI). Paying down bills to less than 30% will result in a considerable increase in credit scores.

Important Actions to Take When Purchasing a Home With Bad Credit

When purchasing a property with terrible credit, following these steps will help you figure out where you are and what to do!

Be Prepared to Pay a Higher Mortgage Interest Rate

A low credit score indicates to lenders that you are a larger risk. To compensate for the risk, any loan proposals they make will normally have a higher interest rate (e.g., a 5% yearly interest rate instead of 3% with a strong credit score).

These single-digit variances may seem minor, but they pile up throughout a mortgage, which typically lasts 15 to 30 years. You may have to pay a greater monthly mortgage payment as a result.

Increase the Amount of Your Down Payment If Possible

A down payment is usually required to receive financing for a house purchase. According to the National Association of Realtors (NAR), the typical house buyer puts down 12% on a property.

If you have poor credit, having a down payment is even more important. When your credit score falls below a specific level, your lender may ask for a higher down payment than normal. Furthermore, putting more money down may make a lender more willing to offer you money despite your poor credit score.

Lower Your Debt-to-income Ratio

The link between your previous obligations and your income—or your debt-to-income (DTI) ratio—is another aspect that influences your ability to qualify for a mortgage. Your DTI ratio shows the lender how much you spend about how much you earn.

In general, the smaller your DTI ratio, the better from a lender’s perspective. For example, if you want to get a new house loan, you’ll usually need a DTI of 50% or less. However, depending on the loan type and other criteria, the maximum DTI ratio that a lender would take might vary.

Conclusion

Simply because you may purchase a property with terrible credit does not mean you should. Working to repair your credit may save you money and make the house purchasing process much more bearable if you have the choice to wait. Furthermore, the time it takes to raise your credit score might be used to pay off bills or save for a bigger down payment.